Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How to Price Real Estate

Posted: 06 Mar 2014 04:00 AM PST

Today we are excited to welcome back Ashley Garner as our guest writer today. Ashley has been a broker for over 20 years in the Wilmington, NC area. – The KCM Crew

Location may have the most effect on value but Price is without question the most important factor controlling the sale of real estate. Anything will sell anytime, how long will it take depends on the price.

Location may have the most effect on value but Price is without question the most important factor controlling the sale of real estate. Anything will sell anytime, how long will it take depends on the price.

Think about it this way – you may really want to buy a car for your collection and your favorite happens to be a 1963 Corvette. So you hear about one for sale, in mint condition, across town but the only problem is the price, the owner is asking $150,000! Well, although you really, really want a mint condition 1963 Corvette, there is no way you will pay anywhere close to $150,000, in fact you know that the most a 1963 Corvette has ever sold for is about $200,000 and that was for a very rare model, which this one is not.

Because you are a bit obsessed with owning one of these cars you spend almost all of your free time, and some of the time you should be working, searching the internet for available cars. Through this exhaustive search you have become somewhat of an expert on the values of 1963 Corvettes, especially in your town. You happen to know that the particular model for sale across town is worth about $95,000…maybe $100,000. In fact, if the asking price was $100,000 or even $110,000 you would’ve driven over there today with your checkbook and driven home in a 1963 Corvette!

So why don’t you go make an offer? Well, let’s face it when you see a price that is so high compared to the actual value it makes you think that the seller is either difficult to deal with and is out of touch with reality or that he must not really want to sell the car, instead he is just fishing for the one fool in the world that will pay $150,000 for a car that is worth $95,000. So you don’t even go look at it or call for more information…you just keep searching the various websites to find the car of your dreams.

Yes, you guessed it the Corvette in this example actually represents your home or other real estate you might be trying to sell. (in fact it represents any item that can be bought and sold).

Wiggle room = Bad idea

Most sellers think that it is necessary to “leave a little wiggle room” in the price. They think this because they think that all buyers will make aggressively low offers…no matter what the asking price. WRONG!!

Buyers pay the fair market value …in other words they will pay you what it is worth! Your job is to find out what it is worth and price it at or near that value.

This is where brokers and/or appraisers come into the picture. The right way to price your property is to have a professional REALTOR/broker or appraiser prepare a CMA (Comparative Market Analysis) on your property. A CMA involves finding recent sales of similar properties, adjusting for any differences, to arrive at a current market value of your property. Once you have this value you should have your broker set the asking price no more than 3% to 5% higher than that current market value.

If you do this, your property will sell quickly for a price equal to exactly what it is worth, or higher! Buyers as a general rule DO NOT make “low-ball” offers, there are some rare occasions when that happens but the vast majority of initial offers are 5% or less below asking price.

If sellers price their property correctly the buyers will know it immediately because, just like in the Corvette example, buyers spend every spare moment searching the internet for a home, they have made themselves experts on the market value of the particular type of home in the particular area they desire. For this reason the buyer also knows when a property is overpriced. Most buyers will not even go look at a property that is overpriced, they say to themselves “why bother?” they assume that the seller is unreasonable and/or is not truly interested in selling the property.

Yesterday, the Buyer’s Specialist that works for my team and I were showing a house to some buyers who were very motivated had already decided on the neighborhood. The house was well within their price range and met every one of their criteria. As we stood in the kitchen discussing what price we should offer we found ourselves drawn to the fact that the house had been on and off of the market for the last four years!

The conversation immediately turned to “what is wrong with this house?” It turns out that the house hasn’t sold because it was severely overpriced most of that 4 years, it happens to be well priced now but the stigma it carries because of the lengthy time on the market will likely result in it selling for less than it is really worth.

Moral of this whole story is – buyers will pay what it is worth – Seller’s job is to find out what it is worth and set the asking price 3%-5% higher than that number…then sit and wait for the offers to roll in.

Should I Rent If I Can’t Sell?

|

Should I Rent My House If I Can’t Sell It? Posted: 04 Mar 2014 04:00 AM PST

The study cites that many homeowners were able to refinance and “locked in a very low mortgage rate in recent years. That low rate, combined with a strong rental market, means they can charge more in rent than they pay in mortgage each month, so they are going for it.” This logic makes sense in some cases. We at KCM believe strongly that residential real estate is a great investment right now. However, if you have no desire to actually become an educated investor in this sector, you may be headed for more trouble than you were looking for. Are you ready to be a landlord? Before renting your home, you should answer the following questions to make sure this is the right course of action for you and your family. 10 Questions to Ask BEFORE Renting Your Home 1.) How will you respond if your tenant says they can’t afford to pay the rent this month because of more pressing obligations? (This happens most often during holiday season and back-to-school time when families with children have extra expenses). 2.) Because of the economy, many homeowners can no longer make their mortgage payment. What percent of tenants do you think can no longer afford to pay their rent? 3.) Have you interviewed a few experienced eviction attorneys in case a challenge does arise? 4.) Have you talked to your insurance company about a possible increase in premiums as liability is greater in a non-owner occupied home? 5.) Will you allow pets? Cats? Dogs? How big a dog? 6.) How will you actually collect the rent? By mail? In person? 7.) Repairs are part of being a landlord. Who will take tenant calls when necessary repairs arise? 8.) Do you have a list of craftspeople readily available to handle these repairs? 9.) How often will you do a physical inspection of the property? 10.) Will you alert your current neighbors that you are renting the house? Bottom Line Again, renting out residential real estate historically is a great investment. However, it is not without its challenges. Make sure you have decided to rent the house because you want to be an investor, not because you are hoping to get a few extra dollars by postponing a sale. |

A

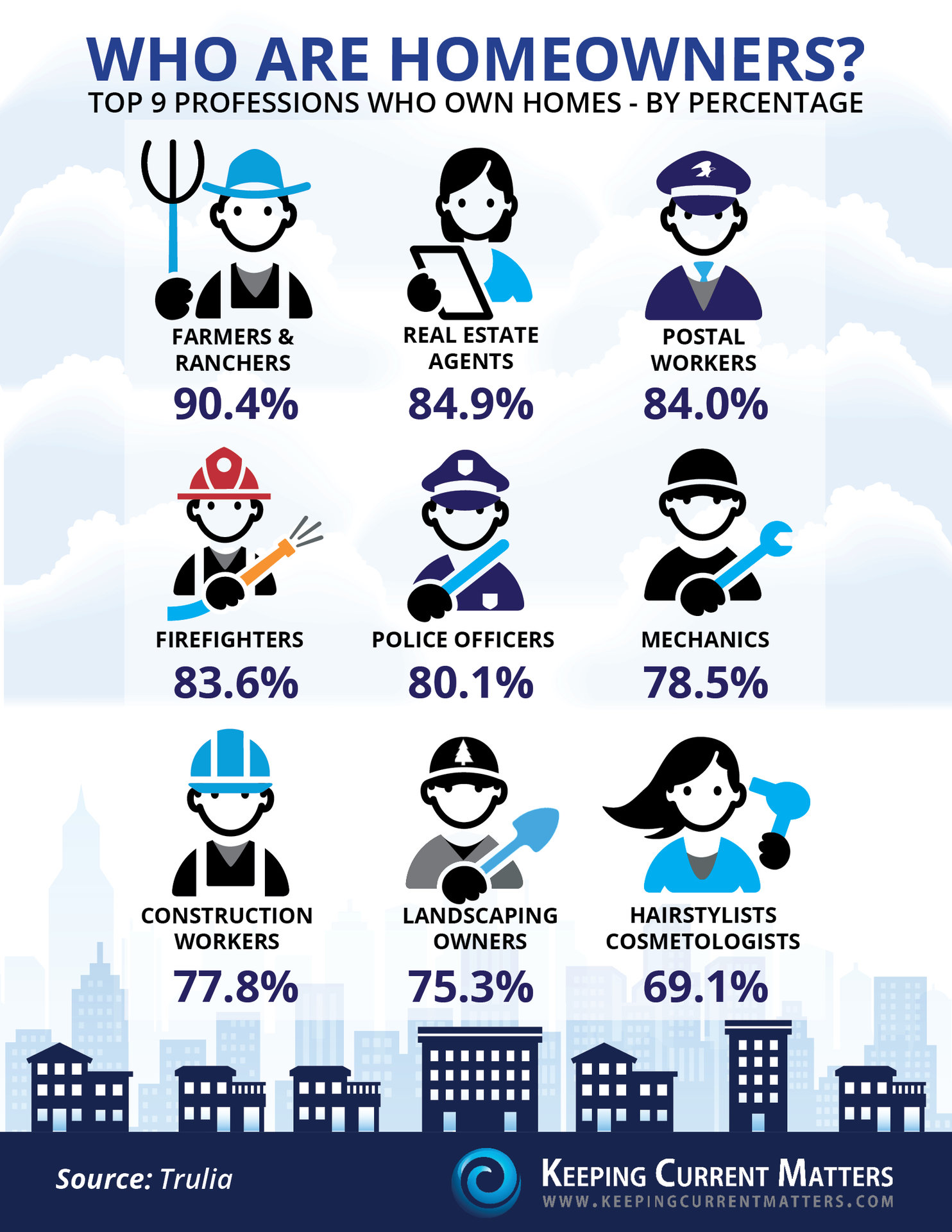

A Who Are Homeowners?

|

Who Are Homeowners? [INFOGRAPHIC] Posted: 28 Feb 2014 04:00 AM PST

|

Just Believe Your Own Eyes

Posted: 26 Feb 2014 04:00 AM PST

Our founder, Steve Harney, occasionally asks to do a personal post on what he sees as important to our industry. Today is one of those days. Enjoy! – The KCM Crew

Many believe the housing market is in a full out recovery. Others are questioning that assumption. To find out, maybe the only thing we need to do is just open our eyes.

Many believe the housing market is in a full out recovery. Others are questioning that assumption. To find out, maybe the only thing we need to do is just open our eyes.

When my wife and I visited Miami ten years ago, we were amazed at the number of building cranes that lined the streets along the beachfront. There was a wave of buyers descending on the city with pockets full of money. Everywhere you looked, there was a new condo complex going up and each building being constructed required a crane on the property. Back then, the city of Miami looked like the set of a Transformer movie with what seemed like hundreds of these huge mechanical machines marching through the city.

Then the housing crisis hit.

Miami property values dropped by over 50%. The buying frenzy cooled.

The cranes disappeared.

Today, Miami’s house prices are beginning to rebound quite nicely. We purchased a condo in South Beach two years ago and have been happy to experience a nice bump in value already. However, this week we realized the Miami market is definitely back. Why do we know this?

The cranes are back.

From the balcony of our waterfront home we can look at the city skyline. This week we saw a familiar sight. Building cranes dotted that skyline. New buildings are being built. There is a new buzz in Miami. Things are the way we remember them being ten years ago.

It seems the market is back!

Buying a Home: Should You Do it Now or Later?

|

Buying a Home: Should You Do it Now or Later? Posted: 11 Feb 2014 04:00 AM PST

Interest rates have remained relatively stable since the onset of the tapering in December. This is probably because the first round of increases had already been ‘priced into’ the equation last summer when rates skyrocketed by over a full percentage point just on the speculation that tapering would take place later in 2013. However, as we move forward, most analysts believe rates will start to rise culminating in a rate close to a full percentage point higher than current rates by this time next year. For example, Freddie Mac, Fannie Mae, The Mortgage Bankers’ Association and the National Association of Realtors have all recently projected rates to be between 5-5.4% at this time next year. Bottom LineIf you are a first time buyer or a move-up buyer, the cost of the mortgage on your new home will probably increase as we move through the year. If the timing makes sense, buying sooner rather than later may save you a substantial amount of money over the long term in lower mortgage payments. |

Last month, the Federal Reserve, in a unanimous vote, decided to further decrease its bond purchasing. The bond purchases were the government’s stimulus package created to keep long term mortgage interest rates artificially low in order to help drive the housing market. Most experts believe that tapering will cause interest rates to increase as we move through the year.

Last month, the Federal Reserve, in a unanimous vote, decided to further decrease its bond purchasing. The bond purchases were the government’s stimulus package created to keep long term mortgage interest rates artificially low in order to help drive the housing market. Most experts believe that tapering will cause interest rates to increase as we move through the year.Be Quiet Chicken Little, The Sky is NOT Falling!

|

Be Quiet Chicken Little. The Sky is NOT Falling Posted: 10 Feb 2014 04:00 AM PST

MORTGAGE INTEREST RATESASSUMPTION: Rising interest rates have forced buyers back onto the fence. Evidence offered up by those in this camp comes directly from the EHS Report from NAR. Three of the last four reports revealed that sales were below sales from the same month the previous year. THE REALITY: Though it is true year-over-year sales have fallen nationally, a closer look at the report reveals major regional differences. Sales in the West Region are down 10.7% versus the same month last year. Sales in the Midwest Region are also down but by less than 1%. The Northeast Region is up 3.2% and the Southern Region is up 4.6%. If the issue is interest rates, why is one region virtually unchanged and two of the remaining three regions up in sales? We don’t believe rates are the challenge. CONSUMER CONFIDENCE in REAL ESTATE is ERODINGASSUMPTION: The pace of the recent price increases has caused many to fear the emergence of a new housing bubble. Similar to the first assumption, evidence offered up by those in this camp comes directly from the less than enthusiastic EHS Reports from NAR. THE REALITY: As we mentioned before, sales in the Midwest Region are down but by less than 1%. The Northeast and the Southern Region have both shown increased sales as compared to the year before. Are only the consumers in the Western Region afraid of a possible bubble forming? The fear of a new housing bubble is vastly overstated. Forty states have not yet returned to home values they experienced seven to nine years ago. Nineteen of those forty states still have home prices 15% or more below peak prices. We believe home values will continue to increase but just at a slower rate of appreciation. It is not just us that believe this is the case. The over 100 housing experts recently surveyed by Pulsenomics revealed that they believe prices will continue to appreciate at historical annual numbers (3-4%) for at least the next five years. THEN WHAT IS THE CHALLENGE?If the lack of sales is not the result of increasing interest rates or decreasing consumer confidence, what actually is happening? We believe it can be broken down to three words: LACK of INVENTORY. Inventories of foreclosure and short sale properties are falling like a rock in the vast majority of regions across the nation. These two categories of homes have driven the market for the last few years. As foreclosures and short sales sell, they are not being replaced because the economy has gotten better and more families have regained control of their finances. All fifty states have seen a decrease in the number of homeowners who are seriously delinquent on their mortgage payments with thirty nine states seeing the number shrink by over 20%. This inventory has not yet begun to be replaced by the non-distressed properties in the country. Just this month, NAR revealed that the months’ inventory of homes for sale has dropped to only a 4 month supply. A normal market has between 5-6 months’ supply. This is the main reason home sales are declining in certain regions – there are just not enough houses for sale. BOTTOM LINEWith the economy improving and with homeowners gaining back some equity they lost when prices fell, we believe there will be many homes coming unto the market this spring. A recent survey revealed that 71% of homeowners are at least considering selling their home in 2014. If you are thinking of selling, beating this increased competition to the market before spring might make sense – and might enable you to get the best price possible for your home. |

There has been much speculation about what is causing the falling sales numbers in the most recent Existing Home Sales Reports (EHS) from the National Association of Realtors (NAR). Some have claimed that rising interest rates have scared buyers out of the market. Others have claimed that consumers are just losing confidence in the housing recovery fearing a new bubble may be forming. We want to look at the validity of these two assumptions.

There has been much speculation about what is causing the falling sales numbers in the most recent Existing Home Sales Reports (EHS) from the National Association of Realtors (NAR). Some have claimed that rising interest rates have scared buyers out of the market. Others have claimed that consumers are just losing confidence in the housing recovery fearing a new bubble may be forming. We want to look at the validity of these two assumptions.

5 Things You Probably Don’t Know About VA Loans…

|

5 Things You Probably Don’t Know About VA Loans Posted: 06 Feb 2014 04:00 AM PST We are pleased to welcome Phil Georgiades as our guest blogger today. Phil is the Chief Loan Steward for VA Home Loan Centers, a veteran and active duty military services organization. – The KCM Crew

With this in mind, we would like to debunk the most common myths about VA Loans. Myth 1: The VA loan benefit has a “one time” use.Fact: Veterans and active duty military can use the VA loan many times. There is a limit to the borrower’s entitlement. The entitlement is the amount of loan the VA will guarantee. If the borrower exceeds their entitlement, they may have to make a down payment. Never the less, there are no limitations on how many times a Veteran or Active Duty Service Member can get a VA loan. Myth 2: VA home loan benefits expire if they are not used.Fact: For eligible participants, VA mortgage benefits never expire. This myth stems from confusion over the veteran benefit for education. Typically, the Montgomery GI Bill benefits expire 10 years after discharge. Myth 3: A borrower can only have one VA loan at a time.Fact: You can have two (or more) VA loans out at the same time as long as you have not exceeded your maximum entitlement and eligibility. In order to have more than one VA loan, the borrower must be able to afford both payments and sufficient entitlement is required. If the borrower exceeds their entitlement, they may be required to make a down payment. Myth 4: If you have a VA loan, you cannot lease the home.Fact: By law, homeowners with VA loans may rent out their home. If the home is located in a non-rental subdivision, the VA will not guarantee the loan. If the home is located in a subdivision (such as a co-op) where the other owners can deny or approve a tenant, the VA will not approve the financing. When an individual applies for a VA loan, they certify that they intend on making the home their primary residence. Borrowers cannot use their VA benefits to buy property for rental purposes except if they are using their benefits to buy a duplex, triplex or fourplex. Under these circumstances, the borrower must certify that they will occupy one of the units. Myth 5: If a borrower has a short sale or foreclosure on a VA loan, they cannot have another VA loan.Fact: If a borrower has a claim on their entitlement, they will still be able to get another VA loan, but the maximum amount they would otherwise qualify for may be less. For example, Mr. Smith had a home with a $100,000 VA loan that foreclosed in 2012. If Mr. Smith buys a home in a low cost area, he will have enough remaining eligibility for a $317,000 purchase with $0 money down. If he did not have the foreclosure, he would have been able to obtain another VA loan up to $417,000 with no money down payment. Veterans and Active duty military deserve affordable home ownership. In recent years, the VA loan made up roughly 13% of all home purchase financing. This program remains underused largely because of misinformation. By separating facts from myth, more of America’s military would be able to realize their own American Dream. |

VA loans are the most misunderstood mortgage program in America. Industry professionals and consumers often receive incorrect data when they inquire about them. In fact, misconceptions about the government guaranteed home loan program are so prevalent that a recent VA survey found that approximately half of all military veterans do not understand it.

VA loans are the most misunderstood mortgage program in America. Industry professionals and consumers often receive incorrect data when they inquire about them. In fact, misconceptions about the government guaranteed home loan program are so prevalent that a recent VA survey found that approximately half of all military veterans do not understand it.5 Reasons You Shouldn’t For Sale by Owner (FSBO)

|

5 Reasons You Shouldn’t For Sale by Owner Posted: 05 Feb 2014 04:00 AM PST

Here are five of our reasons:1. There Are Too Many People to Negotiate WithHere is a list of some of the people with whom you must be prepared to negotiate if you decide to FSBO.

2. Exposure to Perspective PurchasersRecent studies have shown that 92% of buyers search online for a home. That is in comparison to only 28% looking at print newspaper ads. Most real estate agents have an internet strategy to promote the sale of your home. Do you? 3. Results Come from the InternetWhere do buyers find the home they actually purchased?

The days of selling your house by just putting up a sign and putting it in the paper are long gone. Having a strong internet strategy is crucial. 4. FSBOing has Become More and More DifficultThe paperwork involved in selling and buying a home has increased dramatically as industry disclosures and regulations have become mandatory. This is one of the reasons that the percentage of people FSBOing has dropped from 19% to 9% over the last 20+ years. 5. You Net More Money when Using an AgentMany homeowners believe that they will save the real estate commission by selling on their own. Realize that the main reason buyers look at FSBOs is because they also believe they can save the real commission. The seller and buyer can’t both save the commission. Studies have shown that the typical house sold by the homeowner sells for $184,000 while the typical house sold by an agent sells for $230,000. This doesn’t mean that an agent can get $46,000 more for your home as studies have shown that people are more likely to FSBO in markets with lower price points. However, it does show that selling on your own might not make sense. Bottom LineBefore you decide to take on the challenges of selling your house on your own, sit with a real estate professional in your marketplace and see what they have to offer. |

Buy Now Don’t Wait for Spring

Posted: 04 Feb 2014 04:00 AM PST

Based on prices, mortgage rates and soaring rents, there may have never been a better time in real estate history to purchase a home than right now. Here are five reasons purchasers should consider buying before the spring market arrives:

Supply Is Shrinking

With inventory declining in many regions, finding a home of your dreams may become more difficult going forward. There are buyers in more and more markets surprised that there is no longer a large assortment of houses to choose from. The best homes in the best locations sell first. Don’t miss the opportunity to get that ‘once-in-a-lifetime’ buy.

Price Increases Are on the Horizon

Prices are projected to appreciate by over 25% from now to 2018. First home buyers will probably pay more both in price and interest rate if they wait until the spring. Even if you are a move-up buyer, it will wind-up costing you more in net dollars as the home you will buy will appreciate at approximately the same rate as the house you are in now.

Owning a Home Helps Create Family Wealth

Whether you are rent or you own the home you are living in, you are paying a mortgage. Either you are paying your mortgage or your landlord’s. The Fed, in a recent study, revealed that the net worth of the average homeowner is 30 times greater than that of a renter.

Interest Rates Are Projected to Rise

The Mortgage Bankers Association, the National Association of Realtors, Freddie Mac and Fannie Mae have all projected that the 30-year mortgage interest rate will be over 5% by the this time next year. That is an increase of almost one full point over current rates.

Buy Low, Sell High

We would all agree that, when investing, we want to buy at the lowest price possible and hope to sell at the highest price. Housing can create family wealth as long as we follow this simple principle. Today, real estate is selling ‘low’ compared to where it will be next year. It’s time to buy.